So you have saved up Rs 50 lakhs. Congratulations! That is a serious sum of money. Now the big question hits you: where do you put it to work for the next 20 years? Should you buy a flat in Ahmedabad's booming Bopal or a villa in Surat's Vesu? Or should you let mutual funds do the heavy lifting? This is the dilemma every Gujarati investor faces. In this post, we will break down how a 50 lakh investment performs over 20 years: property vs mutual funds in Gujarat. I will share real numbers, locality insights, and a few hard truths. Let us dive in.

The Rs 50 Lakh Question: Property or Mutual Funds?

The truth is, both options have their fan clubs. Your uncle in Satellite will swear by real estate. Your CA friend will preach the gospel of SIPs. Who is right? Well, it depends on your goals, risk appetite, and patience. But here is the thing: we are not talking about a small amount. Rs 50 lakhs is life-changing money. So let us look at the math, the emotions, and the ground reality in Gujarat.

Why Gujarat Real Estate Has Always Tempted Investors

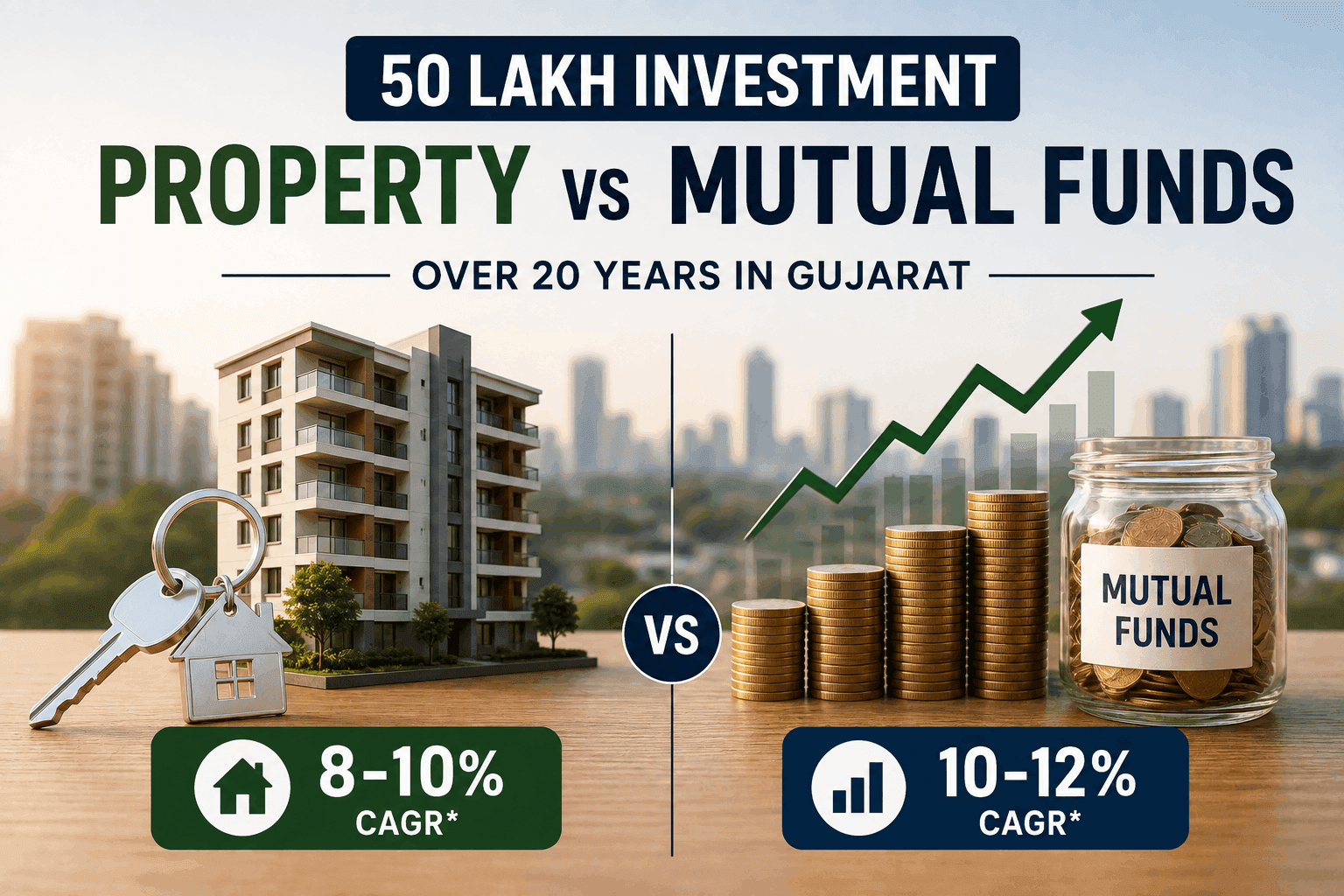

Gujarat has a unique property market. Unlike Mumbai or Delhi, prices here are still relatively affordable. A decent 2BHK in Ahmedabad's Gota or Chandkheda costs between Rs 45-55 lakhs. In Surat, you can get a good flat in Piplod or Althan for Rs 50-60 lakhs. Vadodara's Akota and Gotri offer similar options. The rental yields? Typically 2-3% annually. But capital appreciation has been the real story. Over the past decade, properties in emerging corridors like SG Highway or GIFT City have doubled in value every 7-8 years. However, that pace is slowing. New RERA rules have brought transparency, but also compliance costs. In my experience, the days of 20% annual growth are gone. Still, a well-chosen property in a growing locality can give you 8-10% CAGR over 20 years. That would turn your Rs 50 lakhs into roughly Rs 2.5-3 crores. Not bad, right?

How a 50 Lakh Investment Performs Over 20 Years: Property vs Mutual Funds in Gujarat – The Numbers

Let us get into the nitty-gritty. I have crunched the numbers based on current trends in Gujarat markets.

Scenario 1: Property Investment

Assume you buy a 2BHK in a good society in Shela, Ahmedabad for Rs 50 lakhs (all-inclusive of registration, stamp duty, etc.). Historically, Shela has appreciated at 8% CAGR. Over 20 years, your property would be worth around Rs 2.33 crores. But wait – subtract maintenance costs (society fees, repairs, property tax) which eat into returns. Also, selling a property takes time and brokerage (1-2%). Your net return might be around Rs 2 crores. That is a 4x return. Decent. But here is the catch: liquidity is poor. What if you need money in year 10? You might have to sell at a discount.

Scenario 2: Mutual Funds (Equity + Debt Mix)

Now, put that same Rs 50 lakhs in a diversified equity mutual fund. Historically, Indian equity markets have delivered 12% CAGR over long periods. But let us be conservative and assume 10% CAGR. Over 20 years, your investment would grow to Rs 3.36 crores. That is without any maintenance or selling costs. And you can withdraw partial amounts anytime. However, volatility is real. In a bad year, your portfolio might drop 20%. Can you stomach that? Many investors panic and sell at the bottom. That is the biggest risk.

The Verdict on Pure Returns

On paper, mutual funds win. But life is not lived on paper. Property gives you a tangible asset – a roof over your head or rental income. Mutual funds are just numbers on a screen. Which one feels safer to you?

The Emotional Factor: What Most Calculators Miss

Here is what I tell my clients: investing is 50% math and 50% psychology. Take Ramesh, a first-time buyer from Ahmedabad. He had Rs 50 lakhs in 2015. He bought a flat in Bopal. Today, it is worth Rs 1.2 crores. He also started an SIP of Rs 10,000 monthly in a mid-cap fund. That corpus is now Rs 35 lakhs. He feels proud of his flat. He shows it off. But he never checks his MF portfolio. Why? Because property gives him status. Mutual funds are invisible. That emotional satisfaction matters. But does it justify the lower returns? Not always.

What About Rental Income?

Suppose you rent out your property. In Gujarat, rental yields are low – around 2-3% of property value. On a Rs 50 lakh property, you might get Rs 8,000-12,000 per month. That is Rs 1-1.5 lakhs per year. Over 20 years, that adds up to Rs 20-30 lakhs. But you also have to pay income tax on that. Meanwhile, mutual funds can give dividends or capital gains taxed at 10% for long-term. The math still favours MFs, but rental income provides cash flow. For retirees, that monthly cheque can be a lifeline.

Hidden Costs and Risks You Must Consider

Property Risks in Gujarat

- Liquidity crunch: Selling a flat in Naroda or Vastral can take 6-12 months. In a downturn, even longer.

- Builder delays: Even with RERA, some projects get stuck. Remember the Amrapali fiasco? Gujarat has had its share of stalled projects.

- Legal hassles: Title disputes, encroachment issues, or NOC problems can tie up your money for years.

- Maintenance: A 20-year-old building needs major repairs. That Rs 5 lakh painting job eats into your returns.

Mutual Fund Risks

- Market volatility: A crash in year 19 can wipe out years of gains. But staying invested usually recovers losses.

- Inflation risk: If you choose debt funds, returns may barely beat inflation.

- Behavioural risk: The biggest enemy. You might withdraw early due to fear.

Where Should You Invest in Gujarat Real Estate Today?

If you decide on property, location is everything. In my view, these areas offer the best growth potential for a 20-year horizon:

- GIFT City, Gandhinagar: The next financial hub. Prices are already Rs 8,000-12,000 per sq ft, but expected to double.

- SG Highway extension (towards Sargasan): New developments, metro connectivity, and good rental demand.

- Surat's Vesu and Dumas Road: High-end properties with good appreciation.

- Vadodara's Gotri and Waghodia Road: Affordable entry points with infrastructure growth.

Avoid oversaturated areas like Satellite or Alkapuri – prices are already high and growth is slower.

A Practical Actionable Tip for Today

Here is something you can do right now: Open a comparison spreadsheet. On one side, list the property you are eyeing. On the other, a diversified mutual fund portfolio (60% equity, 40% debt). Assume 8% growth for property and 10% for MFs. Add in maintenance costs, rental income, and taxes. Then ask yourself: Which scenario gives you peace of mind? If you cannot sleep without a physical asset, go for property. If you want flexibility and higher returns, choose MFs. Or better yet – do both! Split your Rs 50 lakhs: Rs 30 lakhs in a flat in Gota and Rs 20 lakhs in a balanced advantage fund. That is diversification done right.

Key Takeaways

- Property in Gujarat can give 8-10% CAGR over 20 years, but comes with high transaction costs and low liquidity.

- Mutual funds historically offer 10-12% CAGR, with better liquidity and lower hassle.

- Emotional comfort matters – do not ignore it.

- RERA registration is mandatory for any property purchase in Gujarat. Always check the RERA number before booking.

- Start small if unsure. Invest Rs 10 lakhs in a good fund and Rs 40 lakhs in a property. See how you feel after a year.

Conclusion: Your 50 Lakhs, Your Future

So, how a 50 lakh investment performs over 20 years: property vs mutual funds in Gujarat – the answer is not black and white. Property gives you a home, status, and stability. Mutual funds give you growth, liquidity, and simplicity. In my two decades of covering this market, I have seen both make millionaires. I have also seen both destroy wealth due to bad decisions. The key is to align your investment with your life goals. Are you buying a home for your family? Go for property. Are you building a retirement corpus? Mutual funds are better. And if you want the best of both worlds? Split your money. Remember, the best investment is the one you can stick with for 20 years. Now go make that decision – your future self will thank you.

*Have questions about specific localities in Ahmedabad, Surat, or Vadodara? Drop a comment below. I reply to every query personally.*