Let me tell you something most financial advisors won't. When you need a large sum of money—say Rs 30 lakhs or more—the first thing many of us think is a personal loan. It is quick, it is unsecured, and the paperwork feels minimal. But here is the truth: for most Gujarat residents, a Loan Against Property in Gujarat: When It Beats a Personal Loan is not just a smarter choice—it is often the only sensible one.

I have seen far too many professionals in Ahmedabad, Surat, and Vadodara rush into high-interest personal loans for business expansion, education, or medical emergencies. They end up paying almost double the amount over five years. Meanwhile, a loan against property (LAP) offers lower rates, longer tenures, and tax benefits. But does it always win? Not always. Let me break it down for you.

What Exactly Is a Loan Against Property?

A loan against property is exactly what it sounds like. You pledge your residential or commercial property as collateral. The bank gives you up to 60-70% of the property's market value. You can use the funds for any purpose—business, marriage, medical, or even buying another property. The loan is secured, so interest rates are much lower than personal loans.

How Does It Compare to a Personal Loan?

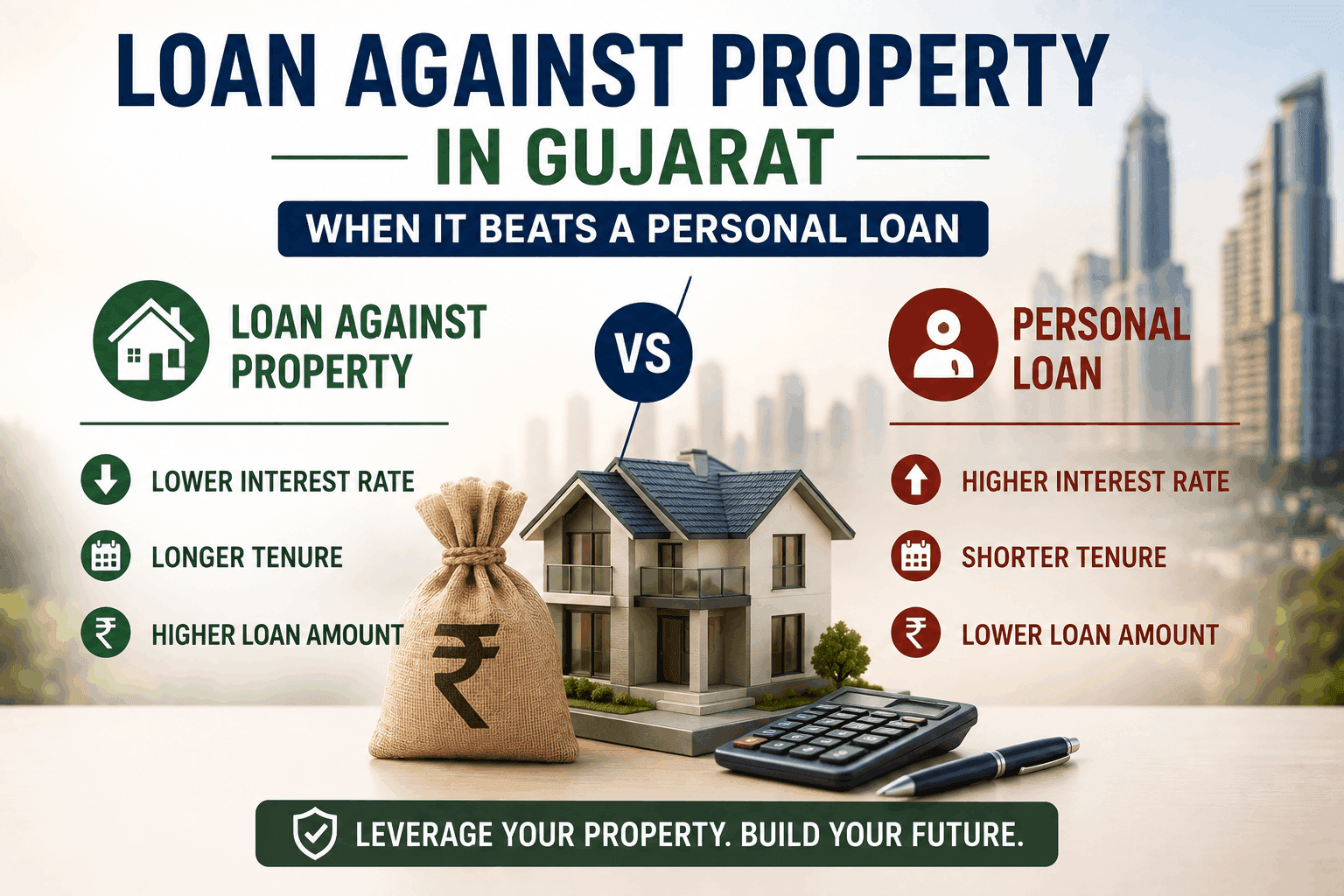

Here is a quick snapshot:

- Interest rates: LAP: 8-10% p.a. | Personal loan: 11-18% p.a.

- Loan amount: LAP: Up to Rs 5 crores or more | Personal loan: Usually capped at Rs 20-30 lakhs

- Tenure: LAP: Up to 15-20 years | Personal loan: 1-5 years

- Processing time: LAP: 7-15 days | Personal loan: 24-48 hours

- Documentation: LAP: Heavy (property papers, valuation) | Personal loan: Light

Now, which one wins? For large amounts, LAP is a no-brainer. But for small, urgent needs, personal loans have speed on their side.

Why Loan Against Property Beats Personal Loan in Gujarat's Real Estate Market

Gujarat's property market has seen steady appreciation. A flat in SG Highway that cost Rs 50 lakhs in 2020 is now worth Rs 70 lakhs. That means you can leverage that equity. In my experience, this is where LAP truly shines.

Lower EMI Burden

Take a Rs 30 lakh loan. At 9% for 15 years, your EMI is around Rs 30,400. A personal loan at 14% for 5 years? EMI jumps to Rs 69,800. That is more than double. For a business owner in Bopal or a doctor in Vesu, Surat, that difference can mean the difference between profit and loss.

Longer Tenure = More Cash Flow

I personally recommend LAP for anyone needing funds for more than 3-5 years. The longer tenure gives you breathing room. You can prepay without heavy penalties in most cases. Many banks in Gujarat, like Bank of Baroda and HDFC, offer zero prepayment charges on floating-rate LAPs after a lock-in period.

When Does LAP Actually Lose to a Personal Loan?

Here is the thing—LAP is not always the winner. If you need Rs 2 lakhs for a wedding or Rs 5 lakhs for a medical emergency, do not pledge your property. The processing fees, valuation charges, and legal costs will eat into the benefit. A personal loan, despite the high interest, makes sense for small, short-term needs.

The Risk Factor

Let me be blunt. If you default on a personal loan, your credit score takes a hit. If you default on a LAP, you lose your home or commercial property. That is a real risk. I have seen families in Naroda and Chandkheda lose their ancestral homes because they over-leveraged. So, only take LAP if you have a stable income and a clear repayment plan.

Gujarat-Specific Insights for Loan Against Property

Ahmedabad Hotspots

Properties on SG Highway, Bopal, and Shela have appreciated 15-20% in the last two years. If you own a flat in these areas, you can get a LAP of Rs 40-60 lakhs easily. Banks love these locations because resale is fast. For a 3-BHK in Bopal worth Rs 80 lakhs, expect a loan of Rs 50-55 lakhs.

Surat's Diamond Zone

In Surat, areas like Vesu, Adajan, and Piplod are prime. A commercial property there can fetch a LAP of up to Rs 1 crore. But remember, commercial properties have higher interest rates (9.5-10.5%) than residential ones (8-9%).

Vadodara and Rajkot

In Vadodara, Alkapuri and Akota have high-value properties. In Rajkot, Kalawad Road and 150 Feet Ring Road are hot. A bungalow in Kalawad Road worth Rs 1.2 crores can give you a LAP of Rs 80 lakhs. That is serious money for business expansion.

RERA Tip You Must Know

Always check that your property is RERA-registered. Banks will not approve a LAP for an unregistered property in Gujarat. Also, ensure the title is clear—no disputes, no pending loans. A quick RERA search online can save you weeks of headache.

Practical Actionable Tip

Before applying, get a property valuation from two different banks. Do not accept the first offer. Banks like SBI, ICICI, and Axis often have different valuation methods. I have seen a difference of Rs 5-10 lakhs in sanctioned amounts for the same property.

Key Takeaways

- Loan Against Property in Gujarat: When It Beats a Personal Loan is clear: for amounts above Rs 10 lakhs and tenures over 3 years, LAP wins on cost.

- Personal loans are better for small, urgent needs under Rs 5 lakhs.

- Always check RERA registration and clear title before applying.

- Compare valuations from multiple banks—do not settle for the first offer.

- Use the longer tenure to keep EMIs low, but prepay when you have surplus cash.

Final Thoughts

So, what is the verdict? If you need a large sum and own property in Gujarat, a Loan Against Property in Gujarat: When It Beats a Personal Loan is the obvious choice. But only if you have a stable income and a clear exit plan. The real estate boom in areas like GIFT City, SG Highway, and Vesu has made LAP more attractive than ever. Do not let the high EMI of a personal loan drain your finances. Instead, leverage your property smartly.

Wondering where to start? Talk to a bank manager or a financial advisor who knows the Gujarat market. And remember—never borrow more than you can comfortably repay. Your home is your biggest asset. Treat it with respect.

*Disclaimer: This is for informational purposes only. Consult a financial advisor for personalized advice.*