Introduction

Are you torn between buying a plot and constructing a home later, or opting for a ready-to-move-in flat? In Gujarat’s bustling real estate market—from Ahmedabad’s SG Highway to Surat’s Vesu—this decision often boils down to financing. Let’s be honest: choosing between a plot loan and a home loan is not just about what you want to buy; it’s about understanding the Plot Loan vs Home Loan: Interest Rate Difference & Hidden Costs. Many buyers overlook the nuances, and that can cost you lakhs. In this guide, I’ll break down the real differences, hidden charges, and practical tips for Gujarat buyers.

What Exactly Is a Plot Loan vs Home Loan?

A home loan is a secured loan for purchasing a residential property—be it a flat, bungalow, or row house. The property is your collateral. On the other hand, a plot loan is specifically for buying a piece of land (residential or commercial). Sounds simple, right? But here is the catch: the rules, interest rates, and hidden costs differ significantly.

Key Differences at a Glance

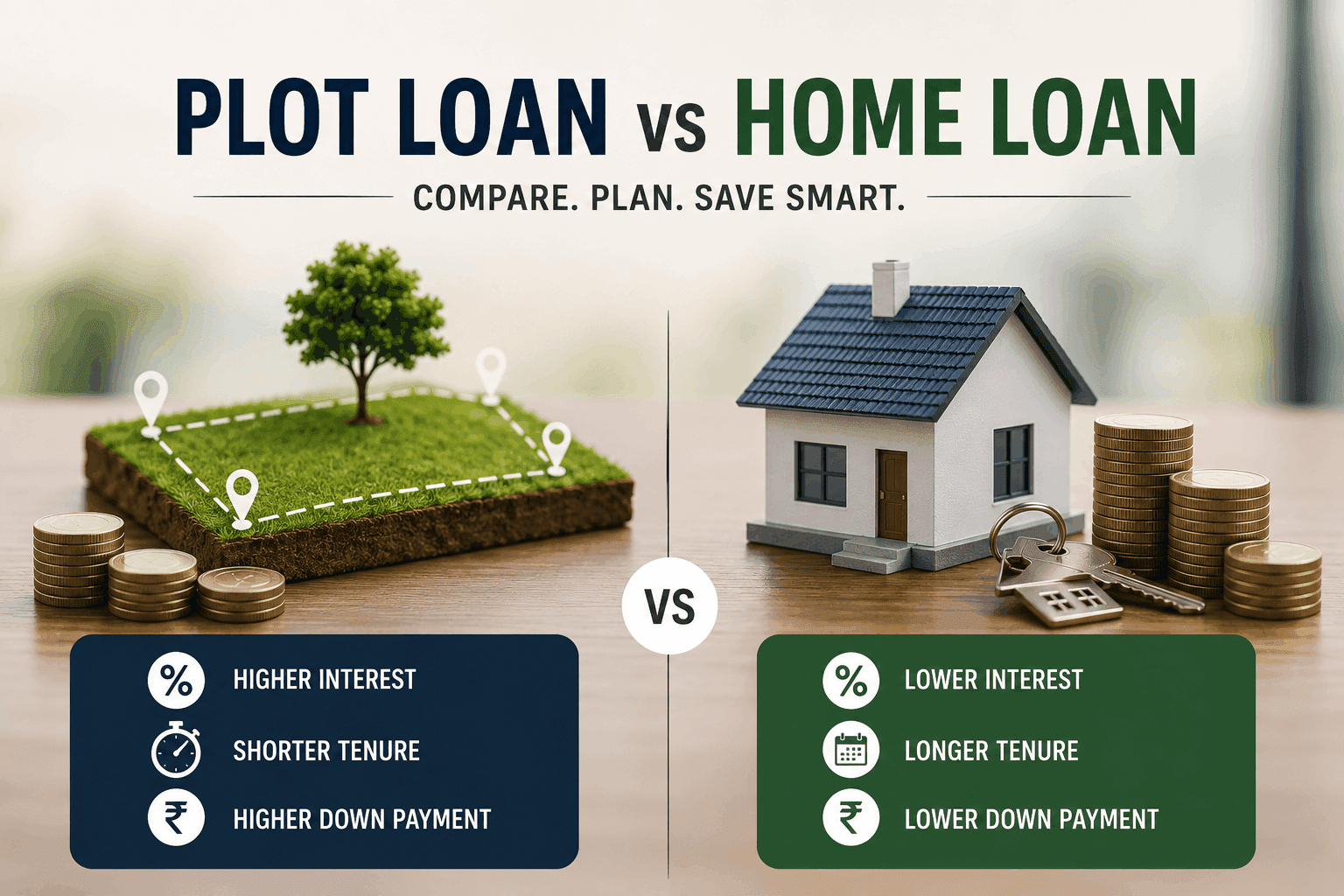

- Loan-to-Value (LTV) Ratio: For home loans, banks typically offer up to 80-90% of the property value. For plot loans, it’s lower—usually 70-75% of the plot’s value. That means you need a bigger down payment for a plot.

- Interest Rates: Home loans often have lower interest rates (8.5-9.5% currently) compared to plot loans (9.5-10.5% or more). Why? Because land is considered riskier—it doesn’t generate rental income until construction begins.

- Tenure: Home loans can stretch up to 30 years. Plot loans are usually capped at 15-20 years. This affects your EMI.

Take Ramesh, a first-time buyer from Ahmedabad. He wanted to buy a 1200 sq ft plot in Bopal. The plot cost Rs 60 lakhs. He had Rs 15 lakhs saved. For a home loan, he could borrow up to 90% of a ready property, but for the plot, the bank offered only 75% LTV—Rs 45 lakhs. He had to arrange Rs 15 lakhs extra. That’s a big difference.

The Real Interest Rate Difference

Let’s get into the numbers. As of 2024-25, here is what you can expect in Gujarat:

- Home Loan Rate: 8.5% to 9.5% (for salaried individuals with good credit).

- Plot Loan Rate: 9.5% to 11% (depending on location, borrower profile, and whether the plot is in a developed area).

But wait—there’s more. Banks often charge a spread over their base rate for plot loans. For example, if the repo rate is 6.5%, a home loan might be repo + 2.5%, while a plot loan is repo + 3.5%. That extra 1% compounds over time.

Why the Difference?

- Risk Perception: Land is illiquid. If you default, selling a plot to recover dues is harder than selling a flat.

- No Immediate Use: Banks know you might not start construction for years. That delays their security.

- Development Status: A plot in a developed area like Gota or Shela (Ahmedabad) gets better rates than an undeveloped one in Naroda.

Here is the thing: Many buyers assume the interest rate is the only cost. But hidden costs can eat into your savings.

Hidden Costs You Must Know

1. Processing Fees

Home loans: 0.25% to 0.5% of the loan amount. Plot loans: 0.5% to 1%. On a Rs 50 lakh loan, that’s Rs 12,500 extra.

2. Legal and Valuation Charges

Banks insist on a legal check of the title deed and valuation of the plot. For a home loan, this is often bundled. For a plot loan, you may pay separately—Rs 5,000 to Rs 15,000.

3. Prepayment Penalties

Some banks charge 2-3% if you repay a plot loan early. Home loans usually have no penalty for floating rate loans. Always check the fine print.

4. Stamp Duty and Registration

On a home purchase, stamp duty in Gujarat is 4.9% for men and 4.9% for women (with a 1% rebate for women in some areas). For a plot, it’s the same percentage, but the base value is often higher per sq yard. In prime areas like Surat’s Adajan, stamp duty can be Rs 2-3 lakhs extra.

5. Construction Timeline Clause

Many plot loans require you to start construction within 3-5 years. If you delay, the bank may increase the interest rate or impose penalties. That’s a hidden trap.

Wondering where to invest? In my experience, a plot in a developing zone like GIFT City (Gandhinagar) or Vesu (Surat) can appreciate faster, but the financing is trickier.

Pros and Cons: Which One Should You Choose?

When to Choose a Home Loan

- You want immediate possession of a ready-to-move-in flat.

- You have a lower down payment (10-20%).

- You want lower EMIs and longer tenure.

- You need tax benefits under Section 80C and 24(b).

When to Choose a Plot Loan

- You want to build a custom home later.

- You have a higher down payment (25-30%).

- You are okay with higher interest rates and shorter tenure.

- You believe the plot will appreciate significantly (e.g., in upcoming metro corridors).

Let me give you a real example. In Vadodara, a plot in Akota costs around Rs 80 lakhs for 2000 sq ft. A home loan for a flat in the same area might be Rs 60 lakhs. If you take a plot loan at 10.5% for 15 years, your EMI is Rs 73,000. For a home loan at 9% for 20 years, the EMI is Rs 54,000. That’s a difference of Rs 19,000 per month. But if the plot value doubles in 5 years, the higher risk pays off.

Tax Benefits: What You Need to Know

This is where many buyers get confused. Here is the truth:

- Home Loan: You can claim up to Rs 1.5 lakh under Section 80C (principal repayment) and up to Rs 2 lakh under Section 24(b) (interest payment). That’s a total benefit of up to Rs 3.5 lakh per year.

- Plot Loan: No tax benefit until you start construction. Once you build, the loan becomes a home loan, and you can claim benefits. But during the plot-only phase, you get zero deduction.

So if you buy a plot and delay construction for 3 years, you lose out on tax savings worth Rs 10.5 lakhs. That’s a hidden cost.

RERA Tip: Always check if the plot is RERA-registered. In Gujarat, RERA registration is mandatory for plots over 500 sq m. Unregistered plots can lead to legal issues. I personally recommend buying only RERA-approved projects.

Practical Tips for Gujarat Buyers

1. Check Your Credit Score: For a plot loan, lenders are stricter. A score of 750+ is ideal. If it’s lower, expect a higher rate.

2. Compare Multiple Banks: Don’t settle for your existing bank. For example, SBI offers home loans at 8.5% but plot loans at 9.5%. HDFC might be 9% and 10% respectively. Use online calculators.

3. Negotiate Processing Fees: Some banks waive processing fees for home loans. For plot loans, ask for a discount—especially if you have a good relationship.

4. Look for Construction-Linked Plans: Some lenders offer a combined loan—first for the plot, then for construction—with blended interest rates. This can save you money.

5. Location Matters: In Ahmedabad, plots in Shela and Bopal have seen 15-20% appreciation in 2024. In Surat, Vesu and Piplod are hotspots. But financing is easier for plots in developed areas.

Key Takeaways

- Interest Rate: Plot loans are 1-2% higher than home loans.

- Hidden Costs: Processing fees, legal charges, prepayment penalties, and stamp duty can add 3-5% extra.

- Tax Benefits: Home loans offer immediate tax savings; plot loans don’t until construction.

- Down Payment: Plot loans need 25-30% down payment vs 10-20% for home loans.

- Tenure: Home loans up to 30 years; plot loans up to 15-20 years.

Conclusion

So, which one is right for you? It depends on your financial situation, timeline, and risk appetite. If you need a home now and want tax breaks, a home loan is your best bet. If you’re planning for the long term and can afford a bigger down payment and higher EMIs, a plot loan can be a wealth-building tool.

But don’t rush. The Plot Loan vs Home Loan: Interest Rate Difference & Hidden Costs can make or break your investment. My advice? Sit down with a financial advisor—or a trusted real estate agent who knows Gujarat’s micro-markets. Check RERA compliance. And always read the fine print.

Ready to make a decision? Start by checking your eligibility for both loans using an online calculator. Then, visit a few projects in your preferred locality. Whether it’s a flat in Gandhinagar’s Infocity or a plot in Rajkot’s Kalawad Road, the right choice will align with your goals.

Have questions? Drop them in the comments—I’d love to help.