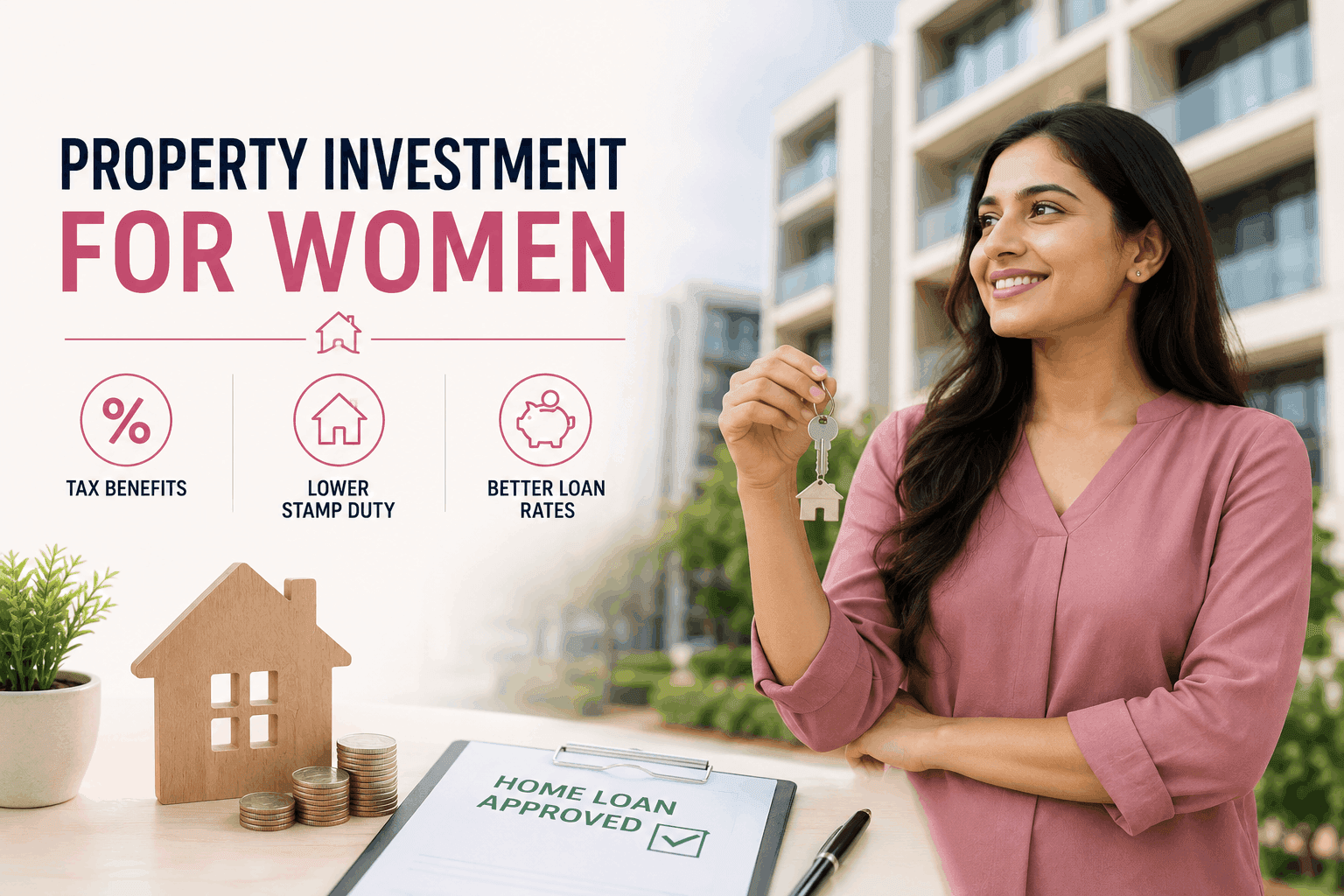

Why Women Should Consider Property Investment in India Right Now

Let me start with a simple truth: property investment for women in India is no longer just about owning a home—it’s about building wealth, securing independence, and leveraging smart tax advantages. In my 15 years covering Gujarat’s real estate market, I have seen a dramatic shift. Take Ramesh, a first-time buyer from Ahmedabad. Wait, that’s not the right example. Let me tell you about Priya, a software professional from SG Highway. She bought a 2 BHK flat in Bopal for Rs 52 lakhs in 2022. Today, that property is worth Rs 68 lakhs. But the real story? She saved nearly Rs 1.5 lakhs in stamp duty just because she bought it in her name. That is the power of being a woman investor.

But what does this mean for you? Whether you are a salaried professional in Surat, a businesswoman in Vadodara, or a homemaker in Rajkot, the current market offers unique opportunities. In fact, many developers in Gujarat—like Savvy Group in Ahmedabad and Shashwat Group in Surat—now offer special discounts for women buyers. The truth is, the government has created a favorable ecosystem for women property buyers. From lower stamp duty rates to preferential home loan terms, the benefits are substantial.

Here is the thing: most women I advise still hesitate. They think property is too complex or too expensive. The reality is, with the right approach, you can start with as little as Rs 5-10 lakhs as down payment in areas like Chandkheda or Vastral in Ahmedabad, or Vesu in Surat. So, let’s break down everything you need to know.

Property Investment for Women in India: Tax Benefits You Cannot Ignore

Section 80C Deductions: The Obvious One

Under Section 80C of the Income Tax Act, you can claim a deduction of up to Rs 1.5 lakhs on the principal repayment of your home loan. But here is what many buyers overlook: this benefit is available to both individual women and joint owners. In my experience, if you are a co-borrower with your spouse, you can each claim the deduction separately. That means a combined saving of up to Rs 3 lakhs per year!

Section 24(b): Interest on Home Loan

Now, this is where the real money is. Under Section 24(b), you can claim a deduction of up to Rs 2 lakhs on the interest paid on your home loan. But wait—there is a catch. This deduction is only available if the construction is completed within five years from the end of the financial year in which the loan was taken. So, if you are buying an under-construction property in Shela, Ahmedabad, make sure the builder delivers on time.

Additional Deduction for First-Time Women Buyers

This is a game-changer. The government introduced an additional deduction of Rs 1.5 lakhs under Section 80EE for first-time home buyers, provided the loan amount is up to Rs 35 lakhs and the property value is up to Rs 50 lakhs. For women, this is particularly beneficial. I personally recommend checking if you qualify—especially if you are looking at affordable housing projects in areas like Naroda or Gota.

Home Loans for Women: Lower Interest Rates and Better Terms

The Gender Advantage

Here is a fact that surprises many: several banks and housing finance companies offer home loans to women at interest rates that are 0.05% to 0.10% lower than those offered to men. It may not sound like much, but on a Rs 50 lakh loan over 20 years, that can save you Rs 1-2 lakhs in total interest. Banks like SBI, HDFC, and ICICI have special schemes for women borrowers.

Processing Fees and Documentation

What many buyers overlook is that processing fees are often waived or reduced for women applicants. For instance, SBI’s ‘SBI Home Loan for Women’ scheme charges no processing fee. Additionally, the documentation is simpler—you just need your PAN card, Aadhaar, income proof, and property documents. In my view, this makes the process far less intimidating.

Joint Loans and Co-Borrowing

If you are married, consider taking a joint home loan with your spouse. Not only does this increase the loan eligibility, but both of you can claim tax benefits separately. I have seen couples in Adajan, Surat, use this to save over Rs 4 lakhs in taxes annually. But here is a tip: ensure the property is registered in both names to claim the benefits.

Stamp Duty Benefits for Women in Gujarat

Lower Rates: The Real Incentive

This is perhaps the most significant financial advantage. In Gujarat, the stamp duty for women buyers is 4.9% of the property value, compared to 5.9% for men. That is a 1% difference. On a property worth Rs 60 lakhs in Alkapuri, Vadodara, you save Rs 60,000 immediately. In fact, many states offer similar concessions—Delhi and Rajasthan have 2% lower rates for women.

How to Ensure You Get the Benefit

To avail the lower stamp duty, the property must be registered solely in the name of a woman or jointly with a woman as the first owner. If you are buying with your husband, make sure your name appears first in the registry documents. I have seen cases where buyers lost the benefit because of incorrect documentation. Always consult a local lawyer or RERA agent.

Registration Charges

In Gujarat, registration charges are typically 1% of the property value, with a cap of Rs 30,000. For women, some sub-registrar offices offer additional concessions, though this varies. My advice: always ask the developer or your agent about any ongoing schemes. For instance, during the recent ‘Gujarat Real Estate Summit’, the government announced a 50% rebate on registration fees for women buying affordable homes.

Legal Rights and RERA Protection for Women Buyers

RERA Registration: Your Safety Net

Under the Real Estate (Regulation and Development) Act, 2016, all residential projects must be registered with RERA. For women buyers, this is a blessing. If a builder delays possession, you can file a complaint and get compensation. In Gujarat, RERA has been particularly active. I recall a case in Gandhinagar’s GIFT City area where a women’s group got full refunds with interest after a builder failed to deliver.

Joint Ownership and Succession

Here is something I tell all my women clients: always insist on being a co-owner if you are contributing financially. Under the Hindu Succession Act, 1956, daughters have equal rights to ancestral property. But for self-acquired property, registration is key. If you are a single woman, consider adding a nominee to avoid legal hassles later.

Practical Tips for Women Property Investors in Gujarat

Start with Affordable Localities

You don’t need to buy in premium areas. In Ahmedabad, localities like Bopal, Shela, and Gota offer great value. A 2 BHK in Bopal costs Rs 50-65 lakhs, while in Shela, you can get a similar flat for Rs 45-55 lakhs. In Surat, Vesu and Piplod are hot picks, with prices ranging from Rs 60-80 lakhs for a 2 BHK. In Vadodara, Gotri and Sama offer good options at Rs 40-55 lakhs.

Check Builder Reputation

Always verify the builder’s RERA registration number. In Gujarat, you can check it on the Gujarat RERA website. I personally recommend sticking with reputed developers like Adani Realty, Savvy, or Shashwat for peace of mind.

Negotiate Like a Pro

Women often hesitate to negotiate, but here is the thing: developers are eager to sell to women buyers. Use this to your advantage. Ask for discounts on parking, clubhouse fees, or even a free modular kitchen. I have seen women get 5-10% off just by asking.

Key Takeaways

- Tax Benefits: Claim up to Rs 1.5 lakhs under 80C and Rs 2 lakhs under 24(b). First-time buyers can get additional Rs 1.5 lakhs under 80EE.

- Lower Interest Rates: Women get 0.05-0.10% lower home loan rates from banks like SBI and HDFC.

- Stamp Duty Savings: In Gujarat, women pay 4.9% stamp duty vs 5.9% for men—a 1% saving.

- RERA Protection: Always buy RERA-registered projects for legal safety.

- Start Small: Invest in affordable localities like Bopal, Vesu, or Gotri with down payments as low as Rs 5-10 lakhs.

Conclusion

Property investment for women in India is not just a financial decision—it is an empowerment tool. The tax benefits, lower loan rates, and stamp duty concessions make it a no-brainer. In my view, every woman should consider owning property, whether for self-use or investment. The Gujarat market, with its robust infrastructure and growing demand, offers excellent opportunities.

So, what are you waiting for? Start your research today. Visit a few projects in your city, talk to a RERA-registered agent, and calculate your EMI. Remember, the best time to invest was yesterday. The next best time is now.

*Disclaimer: This article is for informational purposes only. Consult a tax advisor or real estate professional for personalized advice.*