So, you are a young professional in Gujarat—maybe working at a startup in GIFT City, a tech firm in SG Highway, or a textile company in Surat—and you are dreaming of owning your own flat. But here is the problem: your income today is solid, but it is going to jump significantly in the next few years. A standard home loan feels like a financial straitjacket, locking you into high EMIs right now. What if there was a way to start with lower EMIs and increase them as your salary grows? Enter the Step-Up Home Loans for Young Gujarat Professionals: How They Actually Work. This is not a gimmick. It is a legitimate financial product designed for people exactly like you—young, ambitious, and on a clear upward trajectory. In this comprehensive guide, I will break down everything you need to know, from the mechanics to the real-world implications for buyers in Ahmedabad, Surat, and Vadodara.

What Exactly Is a Step-Up Home Loan? (And Why It Matters for You)

A step-up home loan, also known as a graduated payment mortgage, is a loan where your EMI payments start low and increase at predetermined intervals—typically every 1 to 3 years. The idea is simple: your earning capacity grows, so your loan repayment grows with it.

Here is the thing: most young professionals in Gujarat—whether you are a 28-year-old software engineer in Vastral or a 30-year-old chartered accountant in Alkapuri—face a common dilemma. You want to buy a home now, but your current EMI affordability is limited. A standard loan forces you to either buy a cheaper property or stretch your budget dangerously thin.

But with a step-up loan, you can afford a better property today. For example, if you earn Rs 60,000 per month today, a bank might approve you for a loan where the EMI is Rs 18,000. But with a step-up loan, you might start with an EMI of just Rs 12,000, and it increases by 10-15% every two years as your income grows.

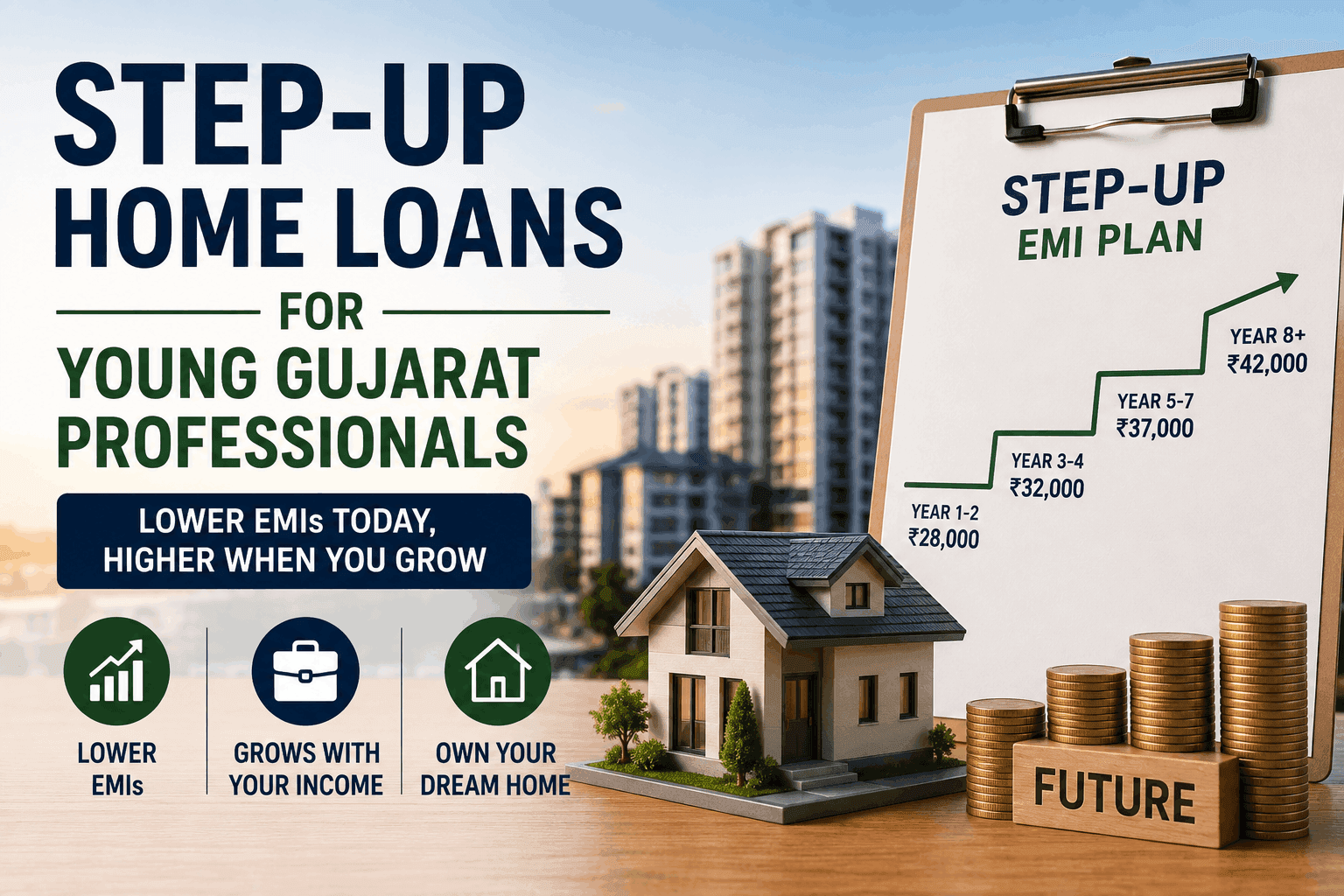

How the Step-Up Structure Works: A Real Example

Let me give you a concrete example. Take Ramesh, a 27-year-old IT professional working in Ahmedabad's SG Highway area. He wants to buy a 2-BHK flat in Bopal worth Rs 55 lakhs. Here is how a step-up loan might look:

- Loan Amount: Rs 44 lakhs (80% LTV)

- Tenure: 25 years

- Interest Rate: 8.5% per annum

- Year 1-2 EMI: Rs 28,000 per month

- Year 3-4 EMI: Rs 32,000 per month (14% increase)

- Year 5-7 EMI: Rs 37,000 per month (15% increase)

- Year 8 onwards: Rs 42,000 per month (fixed thereafter)

The beauty? Ramesh's starting EMI is about Rs 7,000 lower than a standard loan. That extra cash flow allows him to save for furniture, registration costs, or simply live a little. And as his salary grows from Rs 75,000 to Rs 1.2 lakhs over five years, the increasing EMIs feel manageable.

Why Step-Up Loans Are Perfect for Gujarat's Young Professionals

Gujarat's real estate market has unique characteristics that make step-up loans particularly attractive. Let me explain.

Rising Incomes in Key Hubs

Look at the numbers. In Ahmedabad's GIFT City, average salaries for finance and IT professionals have jumped 18-22% year-on-year. In Surat's diamond and textile sectors, young entrepreneurs and managers see income growth of 15-20% annually. In Vadodara's industrial belt, engineers at companies like GSFC and Reliance enjoy steady increments.

So, if your income is going to rise sharply, why not have your home loan EMIs rise in sync? That is the core logic of Step-Up Home Loans for Young Gujarat Professionals: How They Actually Work.

Lower Initial Burden = Better Property Choice

Here is what I tell my clients: with a standard loan, you might be limited to a flat in Chandkheda or Naroda. But with a step-up loan, you could afford that property on SG Highway or in Surat's Vesu area. The initial lower EMI frees up capital for a better location, a bigger flat, or even a down payment.

Tax Benefits That Compound

Under Section 24(b) of the Income Tax Act, you can claim a deduction of up to Rs 2 lakhs on the interest portion of your home loan. With a step-up loan, your interest component is higher in the early years (since the principal is larger). So, you get maximum tax benefit when you need it most—when your income is lower.

Moreover, under Section 80C, the principal repayment also qualifies for deduction up to Rs 1.5 lakhs. So, your effective EMI cost is significantly lower.

The Fine Print: What Banks Don't Tell You About Step-Up Loans

Now, let's get real. Step-up loans sound great, but they have nuances. I have seen many young professionals get excited without understanding the risks.

Eligibility Criteria Are Stricter

Banks do not just hand out step-up loans to anyone. You typically need:

- A proven track record of income growth (at least 3 years of salary hikes)

- A stable job in a high-growth sector (IT, finance, healthcare, management)

- A credit score of 750 or above

- A minimum income of Rs 50,000 per month in most cases

For example, HDFC and SBI have specific step-up products. However, they will ask for your salary slips from the last three years to verify your growth trajectory.

The Total Interest Cost Is Higher

Here is the truth: because you are paying less in the early years, the interest accrues on a larger principal for longer. Your total interest outgo can be 8-12% higher than a standard loan. But here is the counterargument: if that extra cost allows you to buy a property that appreciates 15-20% annually in a hotspot like Shela or Gota, it is a trade-off worth making.

What If Your Income Doesn't Grow as Expected?

This is the biggest risk. Life happens. You might lose your job, face a pay cut, or have unexpected expenses. If you cannot meet the higher EMIs, you could default. Most step-up loans do not have a flexible step-down option.

My advice: Build an emergency fund of at least 6 months of EMIs before opting for a step-up loan. And choose a step-up schedule that is conservative—maybe 10% increase every 3 years instead of 15% every 2 years.

Step-Up vs. Standard Home Loan: A Head-to-Head Comparison

Let me put this in perspective with a real-world scenario for a buyer in Rajkot's Kalawad Road area.

| Feature | Standard Home Loan | Step-Up Home Loan |

|---------|-------------------|-------------------|

| Loan Amount | Rs 40 lakhs | Rs 40 lakhs |

| Tenure | 20 years | 20 years |

| Starting EMI | Rs 34,800 | Rs 28,000 |

| Year 5 EMI | Rs 34,800 | Rs 36,500 |

| Year 10 EMI | Rs 34,800 | Rs 42,000 |

| Total Interest Paid | Rs 43.5 lakhs | Rs 48.2 lakhs |

| Property You Can Afford | Rs 50 lakhs flat | Rs 55 lakhs flat |

See the difference? With a step-up loan, you can afford a property worth Rs 5 lakhs more. In Ahmedabad's Shela area, that extra Rs 5 lakhs could mean the difference between a basic 2-BHK and one with a balcony or a better floor.

Where to Use Step-Up Loans in Gujarat: Hot Localities

Not all areas are ideal for step-up loans. You want a location where property appreciation is strong enough to offset the higher interest cost. Here are my top recommendations:

Ahmedabad

- SG Highway: Prices are Rs 6,000-8,000 per sq ft. Demand is strong due to IT hubs and connectivity. A step-up loan makes sense here because appreciation is 12-15% annually.

- Bopal: A sweet spot for young families. 2-BHK flats range from Rs 50-70 lakhs. The area has good schools and upcoming metro connectivity.

- Shela: An emerging hotspot. Prices are still reasonable at Rs 4,500-6,000 per sq ft. If you buy now with a step-up loan, you could see significant gains in 5 years.

Surat

- Vesu: The most sought-after area. Flats start at Rs 80 lakhs. If you are a young professional earning well, a step-up loan can help you enter this premium market.

- Adajan: Good for mid-range budgets. 2-BHK flats for Rs 45-60 lakhs. The area has good social infrastructure.

Vadodara

- Alkapuri: Premium area with limited supply. Flats cost Rs 1 crore and above. A step-up loan can help you manage the high initial EMI.

- Gotri: An up-and-coming area with prices around Rs 4,000-5,000 per sq ft. Good for long-term investment.

RERA Tip: Protect Yourself

Here is a critical legal tip. Under RERA Gujarat, every project must be registered. Before you apply for a step-up loan, ensure the project has a RERA number. Why? Because if the project is delayed, your step-up loan EMIs will keep increasing even though you are not getting possession. In fact, many banks will not even approve a step-up loan for under-construction projects due to this risk.

My recommendation: Only use step-up loans for ready-to-move-in flats or projects that are at least 80% complete. This way, you avoid the double whammy of rising EMIs and delayed possession.

Quick Tips: Making the Most of Your Step-Up Home Loan

- Negotiate the step-up percentage: Banks often offer standard step-ups of 15-20%. Ask for a customized schedule. I have seen clients negotiate a 10% step-up every 3 years, which is more manageable.

- Prepay when you can: If you get a bonus or a windfall, make a partial prepayment. This reduces the principal and lowers the impact of future step-ups.

- Link it to your career plan: If you are expecting a promotion in 2 years, set your first step-up at that time. If you are in a volatile industry, choose a longer interval.

- Check for hidden charges: Some banks charge a processing fee of 0.5-1% on the entire loan amount. Compare offers from at least 3-4 lenders.

- Use a step-up loan calculator: Most bank websites have these. Play with the numbers to see what works for your budget.

Conclusion: Is a Step-Up Loan Right for You?

So, should you go for a Step-Up Home Loan for Young Gujarat Professionals: How They Actually Work? The answer depends on your confidence in your income growth. If you are in a high-growth field—IT, finance, management consulting—and have a clear career trajectory, it can be a game-changer. It allows you to buy a better home today without sacrificing your lifestyle.

But if you are in a cyclical industry or have uncertain income, stick with a standard loan. The peace of mind is worth more than the extra square footage.

My final advice: Talk to a home loan advisor who understands Gujarat's market. Do not just rely on online calculators. And remember, the best loan is the one you can comfortably repay—whether it steps up or stays flat.

Ready to take the next step? Start by checking your credit score and gathering your salary slips. Then, visit your bank's website and look for their step-up home loan product. The door to your dream home in Gujarat is closer than you think.